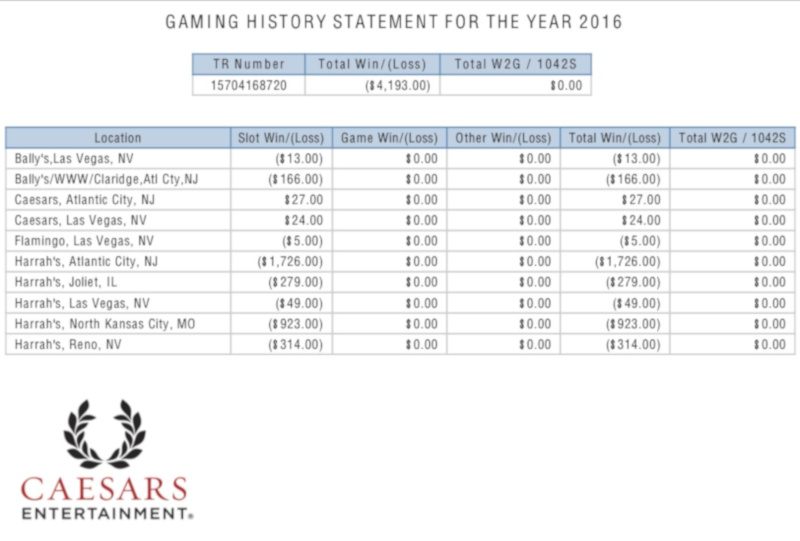

Gamblers love to use casino win/loss statements because it is easy. Just report the amounts from the casino win/loss statements. No muss, no fuss. No record keeping hassles. You’re done.

Unfortunately, it doesn’t work that way.

For starters, the Internal Revenue Code requires taxpayers to keep and maintain adequate records sufficient to prove their income and deductions. In the opinion of the IRS and most courts, casino win/loss statements do not meet these record keeping requirements. And, it is possible, depending upon the facts and circumstances, that the IRS could assess penalties against the gambler that used such documents.

But it gets worse.

The methods the casinos use to calculate your wins and losses – contrary to the “gambling session” method recommended by the IRS – actually overstates these amounts. For example, if you start your IRS-approved gambling session with $100 and end with $125, then you only report $25 of gambling income – according to the IRS-approved “gambling session” method.

On the other hand, if you use your Player’s Card so the casino can track your play – it will. Every winning spin on the slot machine will be recorded, and every losing spin will be recorded. So, if you started with $100 and played for several hours, you could have $2,025 of reportable wins and $2,000 of reportable losses. The net difference is still only $25, but you have to report $2,000 more of income!

Now, comes the really bad part.

Often times the IRS will not challenge the amount of the wins, but they will disallow the gambling losses. So, in our example, the gambler will still be required to report $2,025 of gambling income, but will be prevented from deducting the $2,000 of offsetting gambling losses – the worst of all possibilities!

Because of these problems, it is difficult to recommend that any gambler rely heavily on casino win/loss statements for reporting the amounts of their wagering gains and wagering losses on their income tax return.